Transfer Pricing in KSA – Applicability and Reporting Compliance

On 15 February 2019, the General Authority of Zakat and Tax (‘GAZT’) formally released the final TP Bylaws in the Kingdom of Saudi Arabia (KSA) to ensure the controlled transactions between related parties are more structured and priced fairly and to avoid shifting of profits from one tax jurisdiction to another tax jurisdiction.

What is Transfer Pricing?

Transfer pricing is an exercise involving determination of arm’s length prices in the context of with transactions between related persons (also referred as ‘controlled transactions’) including but not limited to the provision of goods, services, Loans or intangibles. The controlled transactions could either occur between related persons located in the same Tax Jurisdictions or between those located across different tax jurisdictions.

In order to ascertain the fair price for controlled transactions, the Arm’s Length Principle (ALP) is adopted wherein the price charged by one party to its related party under given set of conditions must be the same as if the parties were not related.

Applicable to whom:

The provisions of Transfer Pricing Law is applicable to below person(s) engaged in a controlled transaction with a related party(s) :

- Resident Non-Saudi natural person who conducts business in the KSA. (For purposes of Saudi Income Tax Law, citizens of Gulf Cooperation Council (GCC) are treated as Saudis.)

- Non-resident who conducts business in the KSA through a permanent establishment (“PE”).

- Non-resident with other taxable income from sources within the KSA.

- Person engaged in the field of natural gas investment.

- Person engaged in the field of oil and hydrocarbons production.

- Resident capital companies that are subject to both Income Tax and Zakat (Mixed Companies) but only to the extent of the share of non-Saudi partners.

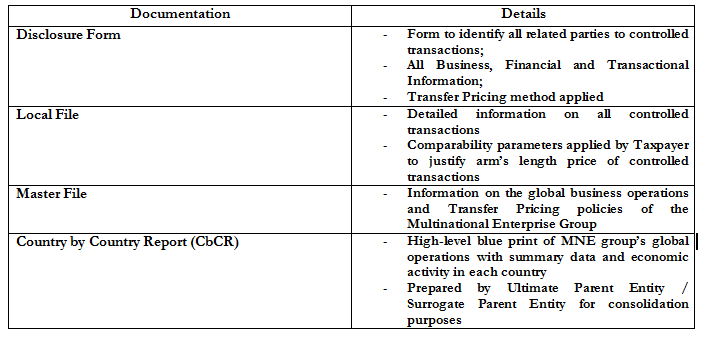

Four Tier Documentation Levels:

The By-Laws requires the taxable persons to comply with the following:

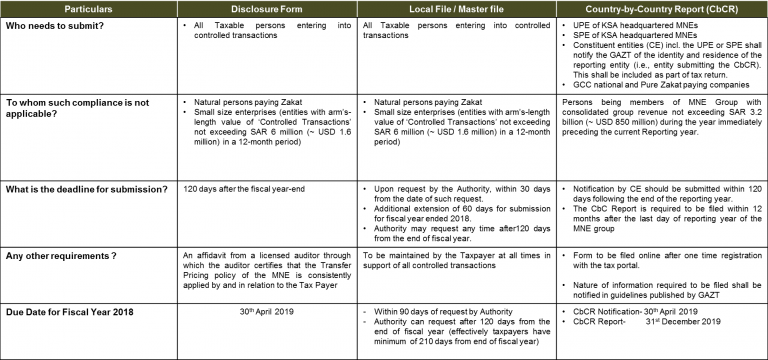

Compliance Requirement:

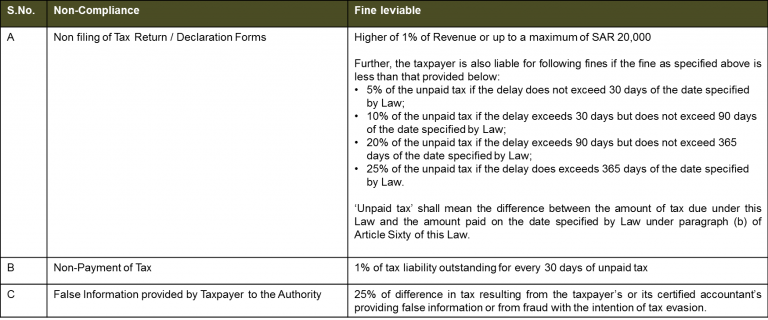

Penalties for Non-Compliance

Suggestion

Regional headquarter of all the companies need to ensure that any Controlled Transaction with the Corresponding related entity in KSA should be complied with the Transfer Pricing Rules by following transfer pricing methods and the documentation requirements for the controlled transactions.

Contact Us for more information

Last Updated: 19th March 2019

This article is contributed by: